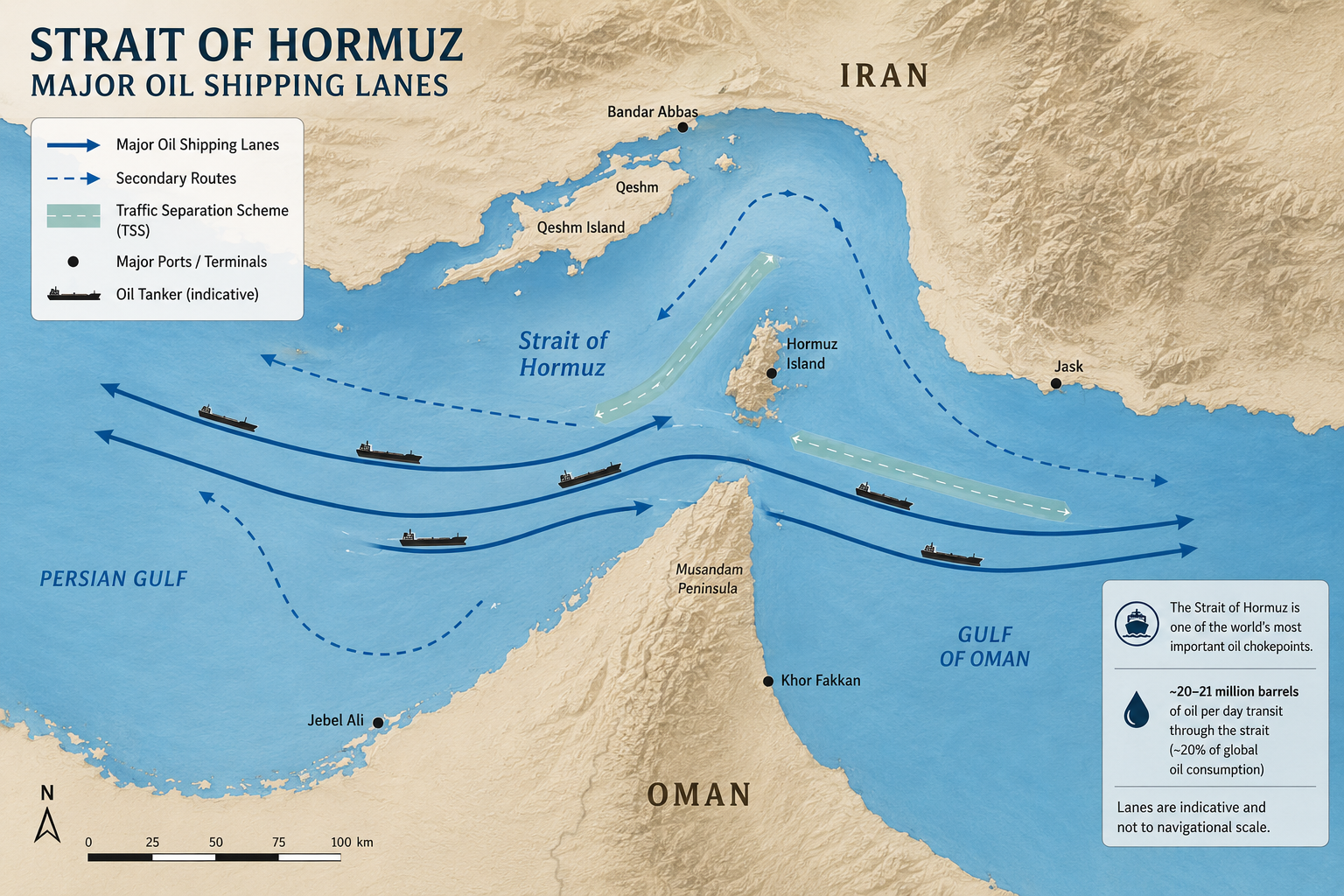

The Strait of Hormuz is one of the most consequential chokepoints in the global economy. Connecting the Persian Gulf to the Gulf of Oman, this narrow waterway barely 33 kilometres wide at its narrowest point serves as the primary maritime corridor for roughly 20% of the world's oil trade. For the UAE, a nation whose prosperity has been built in large part on hydrocarbon exports and trade, the strait is not a distant geopolitical concern but a daily economic lifeline.

Understanding the UAE Strait of Hormuz blockade economic impact requires examining the country's deep structural dependencies: from crude oil exports that fund national development to the imported goods that fill supermarket shelves and power factories. A sustained closure of this passage would not be a minor disruption it would constitute one of the most severe economic shocks the region has ever faced.

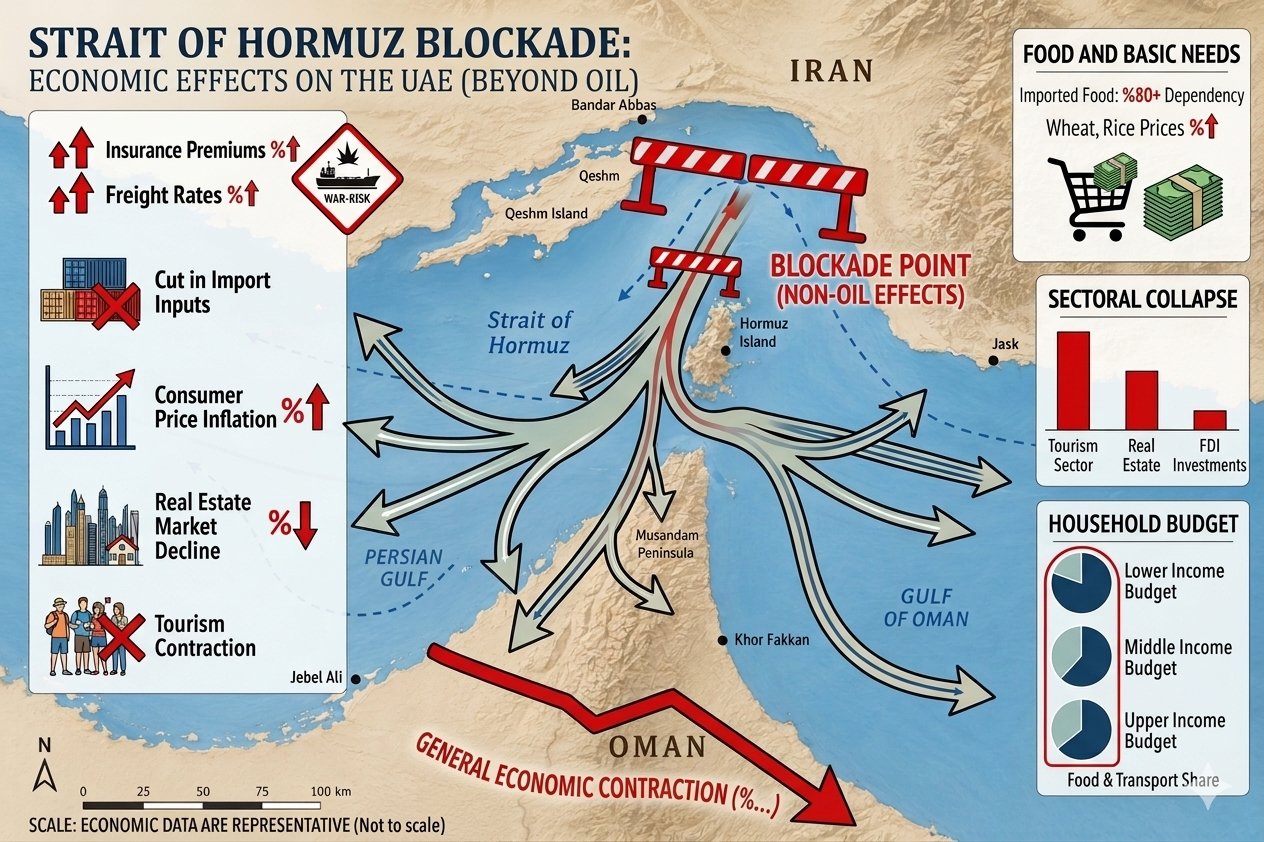

A blockade of the Strait of Hormuz would significantly disrupt the UAE's economy by halting oil exports, driving up import costs, and triggering inflationary pressure across energy, food, and consumer sectors. Government revenues, GDP growth, and foreign investor confidence would all face serious downward pressure.

The Strategic Importance of the Strait of Hormuz

Few maritime passages carry the geopolitical weight of the Strait of Hormuz. According to the U.S. Energy Information Administration, approximately 21 million barrels of oil per day flow through the strait a figure that represents a fifth of total global petroleum liquids consumption. Liquefied natural gas (LNG) exports from Qatar, one of the world's largest LNG producers, also depend almost entirely on this route.

Beyond raw energy volumes, the strait is an artery for container shipping, bulk carriers, and tankers serving economies across Asia, Europe, and beyond. Japan, South Korea, China, and India four of the world's largest energy importers all rely heavily on Gulf supplies routed through Hormuz. Any sustained interruption would cascade through global supply chains within days.

The UAE's Economic Dependence on the Strait of Hormuz

The UAE is not a passive bystander in Hormuz traffic it is one of the passage's most economically invested nations. Abu Dhabi, which holds roughly 6% of the world's proven crude oil reserves, channels the vast majority of its exports through Gulf waters and then through the strait. The UAE's oil and gas sector, though accounting for a declining share of GDP due to active diversification, still contributed approximately 30% of national GDP in recent years and funds a significant portion of federal spending.

Equally important and often underappreciated is the import side of the equation. The UAE imports around 80–90% of its food, along with substantial volumes of manufactured goods, raw materials, and industrial equipment. Much of this arrives via sea routes that pass through or adjacent to the Strait of Hormuz. Understanding how the Strait of Hormuz blockade affects the UAE economy means acknowledging that the vulnerability runs in both directions: exports blocked in, imports blocked out.

Potential Economic Impacts of a Blockade

Disruption to Oil and Gas Exports

The most immediate consequence of a blockade would be the paralysis of hydrocarbon exports. The UAE exported an average of around 2.5–3 million barrels of crude oil per day in recent years, generating revenues that underpin the federal budget, sovereign wealth funds like ADIA, and long-term development plans such as the UAE Centennial 2071. Even a two-week closure could result in tens of billions of dollars in deferred or lost revenue.

The UAE Strait of Hormuz blockade economic impact on government finances would be swift and structural. Oil price spikes globally would occur in parallel potentially offering some revenue windfall for exports that do escape through alternative routes but the volume constraints would outweigh any price premium in the short term. GDP growth projections, currently forecasted in the 4–5% range, could contract sharply depending on blockade duration. The UAE financial impact of Hormuz closure would also affect downstream industries petrochemicals, aluminium smelting, and fertiliser production all of which depend on stable energy input costs and export logistics.

"The Strait of Hormuz is not simply a sea lane it is the economic jugular vein of the Gulf. Any sustained interruption does not merely wound an economy; it changes the calculus of every investor, every shipper, and every government that depends on Gulf energy."

Regional Energy Analyst perspective

Increased Import Costs and Inflation

A blockade does not merely cut exports it detonates import economics. Shipping insurance premiums for Gulf-bound vessels would surge, with war-risk insurance historically spiking 10–20 times baseline rates during regional conflict scenarios. Shipping lines would divert or suspend routes, and those willing to operate would command sharp freight rate premiums.

For the UAE, a nation that imports the bulk of its food staples rice, wheat, poultry, vegetables this translates directly into consumer price inflation. Inflation, already a concern in urban centres like Dubai and Abu Dhabi, could accelerate significantly. The UAE financial impact of Hormuz closure would be felt most acutely by lower and middle-income residents, for whom food and transport represent the highest share of household spending. Fuel costs for re-exported goods and domestic logistics would also rise, compounding inflationary pressure across the board. This is a key dimension of how the Strait of Hormuz blockade affects the UAE economy beyond the headline oil figures.

Broader Economic Consequence

The non-oil economy which Dubai in particular has worked hard to diversify would not be insulated from the shock. Tourism, a pillar of Dubai's economic model, would contract sharply as international visitor confidence declined and airlines reconsidered Gulf routes. Real estate markets, which attract significant foreign capital partly because of the UAE's perceived stability, would face valuation pressure and deal freezes.

Foreign direct investment (FDI), which reached record highs in 2023 and 2024, would slow as investors adopted a wait-and-see posture. Financial services, logistics, and retail all major components of the UAE Strait of Hormuz blockade economic impact picture would register declining activity. The reputational risk to the UAE as a "safe haven" for regional capital could outlast the physical blockade itself, making recovery slower than the disruption.

Mitigation Strategies and Alternative Routes

The UAE has not waited passively for crisis to arrive. The Habshan–Fujairah pipeline also known as the Abu Dhabi Crude Oil Pipeline (ADCOP) was designed precisely to bypass the Strait of Hormuz. Running 380 kilometres from Abu Dhabi's interior oil fields to the emirate of Fujairah on the Gulf of Oman, it has a capacity of approximately 1.5 million barrels per day. While this provides meaningful relief, it covers only around half to two-thirds of the UAE's typical export volume, meaning full bypass remains impossible with current infrastructure.

Beyond pipeline diversification, the UAE's broader economic diversification strategy enshrined in Vision 2030 and Centennial 2071 has been reducing oil dependency as a share of GDP for over a decade. Free zones, financial services, logistics hubs, and technology investment have all grown. Fujairah itself has been developed as a major oil bunkering and storage hub, providing strategic reserve capacity. The UAE financial impact of Hormuz closure would be significantly less severe today than it would have been twenty years ago but it would still be severe. How the Strait of Hormuz blockade affects the UAE economy going forward will depend heavily on how quickly these alternative route capacities can be expanded and how effectively diversification continues.

UAE's Hormuz Bypass & Diversification Milestones

2012

Habshan–Fujairah (ADCOP) pipeline inaugurated, 1.5 mb/d capacity

2016

UAE Economic Vision 2030 accelerated with non-oil targets

2019

Fujairah established as world's second-largest bunkering hub

2022

UAE FDI record broken; non-oil GDP surpasses oil GDP for first time

2024

Renewable energy and hydrogen export infrastructure investment surges

Global Implications of a Blockade

The UAE Strait of Hormuz blockade economic impact would not remain contained within Gulf borders. Global oil markets would react within hours of credible blockade reports. Brent crude prices could spike 30–50% or more in the short term, triggering fuel price increases across importing economies and stoking inflation in regions already managing tight monetary policy.

Asian economies particularly China, Japan, South Korea, and India would face the most acute disruption given their dependence on Gulf oil. European markets, while more diversified in supply, would nonetheless experience energy cost increases. Shipping insurance and freight rates globally would rise as risk appetite contracted. The International Energy Agency (IEA) strategic reserves mechanism would likely be activated, but strategic petroleum reserves offer weeks of cover, not months. In short, how the Strait of Hormuz blockade affects the UAE economy is inseparable from how it affects the global economy the two are tightly coupled.

The UAE Strait of Hormuz blockade economic impact is both enormous in potential scale and more manageable than it once was, thanks to deliberate strategic investment. The country has built pipeline bypasses, diversified its economy, developed Fujairah as an alternative maritime hub, and attracted global capital across non-oil sectors. Yet the underlying exposure remains real: a prolonged blockade would still trigger lost export revenues in the tens of billions, consumer price inflation, reduced foreign investment, and a contraction across tourism, real estate, and financial services.

The fundamental lesson is one of resilience through diversity. The UAE financial impact of Hormuz closure would be far more severe for an economy that had not invested in alternatives. For businesses, investors, and policymakers, the scenario underscores the importance of supply chain redundancy, currency reserve management, and continued non-oil sector development. The strait remains critical but the UAE is working, methodically, to ensure no single chokepoint can define its economic future.

Summarise with AI:

Did you like this article? Leave a rating!